Responsible Investment needs a bigger toolbox

A survey of ESG influencers shows the elusive side of investor responsibility. What to do?

When the Covid-19 crisis exploded in winter 2020, we spelled out four different scenarios for ESG in times of pandemic.

In one scenario, we envisioned that responsible investment could disappear by failing to “show up” in this crucial moment. In another, we thought that on the contrary, it could blow up as the crisis forced a rethink of capital markets and governance. We further considered that the voluntary approaches of business and finance could take an even more dominant role faced with inadequate government response, ushering a new era of hyper-capitalism. We also imagined that a business-as-usual scenario could prevail with ESG continuing to progress on the business side(e.g. asset gathering), but with no marked change in its capacity to alter the course on major systemic issues.

There were many unknowns at time, and many remain, with the pandemic still on the march despite efforts to reopen economies. We have a better sense of the devastating economic impact and of governments’ trillion dollar responses. We’ve seen markets rise and fall, at times clearly disconnected from the real economy – if unemployment is any measure of that (and in the long run, the employment outlook does not look good). We’ve seen social, political and racial tensions explode in various countries amidst volatile political climate compounded by and exacerbated geopolitical tensions.

And we’ve heard calls to build back better, inspired by images of Himalayan summits piercing through after decades shrouded in pollution and responding to a widespread appetite to turn the crisis into opportunity.

On that front, the response is at best mixed so far: even in the progressive European Union, a green tinted Covid-19 EUR 750 billion recovery package, or even the distant hope that a newly minted borrowing capacity could open the door to a carbon tax, stand in contrast to domestic support for aviation and other fossil fuel industries. It looks worryingly like same “old same old.” That battle is not over but the window to effectively turn the crisis into an opportunity won’t be open forever.

The choices that governments make in the coming months will be shaping key environmental and social issues for the foreseeable future. So where do ESG influencers stand within all this?

There has been much rejoicing because ESG funds have done well in terms of performance over the long term, have shown resilience and accelerated inflows during the crisis. And increasingly we are hearing and reading that systemic risks are the next big thing. But a recent Preventable Surprises survey of ESG influencers[1] suggests that we should be guarded about a Covid-19 moment.

What ESG influencers are saying

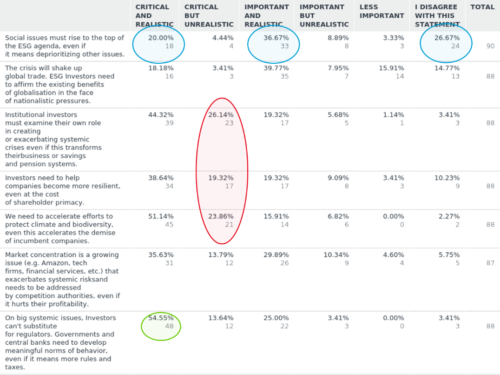

Consider this: our respondents sent important signals about the importance of social workers related issues, with 68% thinking that companies should protect workers at the expense of dividends and bonuses in the short term. In the long term, 60% thought it critical or important for social issues to rise to the top of the ESG agenda, even if it meant deprioritizing environmental or governance issues. However, 25% disagreed with this statement, making it the least consensual response. Several commented that it would be wrong to de-emphasize areas where so much progress has already been made.

Of course, this is a “leading” question – e.g. forcing respondents to make a choice – but it has a rational basis: ESG team resources are limited and frequently stretched. To take on a larger portfolio, more resources are needed. At the same time, another reading of this is to remember that systemic environmental issues and social issues are converging fast, if not inextricable: workers, the poor, minorities and vulnerable populations are the first to suffer from environmental shocks, and social support is essential to fixing systemic crises.

Consider these other results: we asked how respondents rated the importance of examining the role of institutional investors in exacerbating systemic crises, even if it meant changing business models (ca. 90% agreed). We asked if they should help companies become more resilient, even at the cost of shareholder primacy (ca. 86% agreed). We asked if they should accelerate climate and biodiversity efforts, even at the expense of incumbent companies (ca. 97% agreed). All three statements received significant support, but: among that enthusiastic group, a fifth to a quarter thought the propositions to be as unrealistic as they were important or critical.

This should give us pause. Our advisor Bill Baue thinks of it this way:

“If a problem is critical, then, don’t we really NEED to deal with it? What makes it “unrealistic”? In my experience, it is very rare that something is *literally* unrealistic – like, it defies the law of gravity. No, unrealistic is a euphemism for politically inconvenient. So what we have here is a set of critical issues that our political “reality” has deemed inconvenient to solve – often because solving the problem would require transforming the system. ESG in general addresses the “critical but realistic” issues, and leaves the “critical but unrealistic” issues untouched. I think it’s high time for ESG to be recognized as a necessary but insufficient transitional strategy toward more profoundly transformative strategies that are designed to achieve bona fide sustainability (and beyond).”

If the most important set of actions are out of reach, then what one earth does it mean for investor responsibility?

This leads us to two observations:

- If dealing with certain issues is important but unrealistic, then it may be that many ESG teams are not actually empowered to fully handle ESG issues – with crucial levers left to others within their organizations.

- Investors need to expand their ESG toolbox, because their current means are insufficient.

What institutional investors could do

Here are suggestions for empowered teams and expanded tool boxes:

- Asset management leaders need to have open conversations with their ESG teams: beyond AUM, is our strategy working to handle systemic risks? If not, what can be done? How do we turbo-charge our management of systemic risks – from climate to biodiversity to social inequalities – and impact?

- ESG teams’ stewardship capacity needs to grow to cope with a growing array of challenges. Willis Towers Watson thinks investing a quarter of a basis point of assets invested is a good idea.

- ESG teams skill up and integrate with other functions: they learn to assess the macroeconomic dimensions of ESG risks, they learn to assess political risk and understand the social climate.

- Equally, institutional investors accelerate staff diversity efforts. The status quo is wrong, entrenches the disconnect between capital markets and society, and it is destructive.

- Responsible investors adopt systems or holistic thinking to better act on the interplay of environmental and social issues. They look at approaches like the World Benchmarking Alliance or UNEP FI’s Positive Impact Initiative for solutions.

- Responsible Investors become a proactive voice in the post Covid-19 recovery: if governments and companies feel trapped in making difficult environmental and social decisions that involve challenging short and long term trade-offs, then investors need to provide their own vision, on sectors, on global trade and reshoring, including how governments, investors and companies should support Just Transitions.

- Institutional investors openly embrace beta-activism as essential strategy to managing their long term liabilities. They make it part of their asset allocation, following the lead of the Japanese Government Pension Investment Fund.

- Investors embrace new governance models. Some disagree, noting that corporate purpose is a fig leaf, or feel that the German model doesn’t work or can’t be exported, or think that regulation is more important. But let’s let reality speaks for itself: with companies and markets propped up by trillions of public money, we are in a de facto stakeholder model – only: it’s been convinced to behave in shareholder fashion. Should it remain so?

- As institutional investors think about systemic risks, they challenge dominant assumptions that voluntary market forces are the only way to manage them; they look beyond current ESG practice – the change from within – to consider what makes societies and markets resilient and fair, from safety nets to savings and retirement systems, and to their own incentives, governance and business models.

There is always more to systems wide issues, whether cultural or strategic, and we don’t want to infer too much from an imperfect survey. But some questions glaringly need to be asked, and beggar answers. The risk of a second wave, the continued economic shock and massive unemployment, the racial protests and political uncertainties, the multiplying environmental disasters – in short the multiplication of systemic crises or the crash of Gray Rhinos in front of us – makes this urgent.

Sitting back and watching it all crumble is not a viable option. Get in touch if you would like to discuss any of these ideas.

[1] Survey conducted as part of our Breaking the Fever podcast series, in partnership with www.ethicalsystems.org . We reached out to 200 global ESG professionals and executives whose voices we and our network know to have an influence. This blog zooms in on part of the results. See the full survey for more details.