Health, climate and biodiversity: three reasons for investors to confront corporate capture in the chemicals sector

December’s Corporate Lobbying Alignment Project online investor roundtable will tackle corporate capture of public policy making in the chemicals sector, with a focus on agrochemicals and petrochemicals. Companies in both industries are significant contributors to climate change and have actively undermined efforts to reduce emissions and to introduce the precautionary principle into chemicals regulation. In the chemicals sector, investors have an opportunity to engage in three core opportunity areas to support climate action. Global petrochemical and agrochemical value chains have a direct impact on biodiversity loss, and chemical contamination of ecosystems and the environment, with serious health implications for humans. Indeed, according to the WHO, pesticides alone account for around 200,000 acute poisoning deaths each year. Recent lawsuits against Monsanto over its Roundup weed killer illustrate the potential legal risks to investor bottom lines in the sector. These threats are interlinked and have common origins in upstream fossil fuel production of coal, oil, and natural gas, which provide the feedstocks for many chemicals (see a simplified diagram of the relationship below). The sector is dominated by just a handful of companies meaning that investors can engage in sector-wide shareholder resolutions and deploy targeted stewardship tools with global impact.

Systemic risks require systems-wide investor engagement

The chemical sector poses systemic climate change, biodiversity loss and human health risks that cut across market and geographies. Chemical contamination of soil, freshwater, eutrophication in the oceans, and acute air pollution in cities (By 2050, air pollution is projected to become the leading global cause of mortality), all pose challenges for investors. Cross contamination can add more complexity to the risk analysis, with soil co-contaminated with heavy metals and pesticides one example of this. Investors concerned with systemic risks should consider the long-term nature of environmental contamination and bring the precautionary principle into their engagements to drive sector-wide business transitions. This is a net challenge for them, since they’ve historically chosen to focus on single companies or discrete issues. With global bond markets outstanding value at $105 trillion in 2019, and with global equity market capitalisation estimated at $95 trillion, how should these investors engage to support a transition to better products and business models for the global chemical majors?

Moving beyond disclosure to demand transformative practices across the industry

While climate change and greenhouse gas emissions accounting and reporting is a core focus for investor groups including the UN-PRI and ClimateAction100+, the links between upstream fossil fuel production and the downstream petrochemical production are less prominent in stewardship discussions. As policymakers ramp up climate commitments on both sides of the Atlantic, petrochemical and agrochemical company emissions, and their respective lobbying records on climate change, will come under greater scrutiny. This is important and overdue and investors should press for open discussion on how the chemicals sector can address the systemic risks to the environment and human health arising from its products..

Globally around 20 percent of extracted fossil fuels are used for petrochemicals and 24 percent are used for agriculture, which includes manufacturing, production, processing, transportation, marketing, and consumption. Oil, for example, is used to make chlorobenzene, which in turn is used to synthesise the well known pesticide DDT. Similarly, many pesticides such as neonicotinoids, pyrethryoids, and glyphosate formulants are produced from gas and oil. The risks of a petrochemical dependent food production system are well documented, but investors have not yet engaged in a meaningful way to demand changes to either industry.

Concentration in the sector should make engagement easier. ExxonMobil, BASF, Eni, INEOS, and Dow, for example, are the largest plastic producers worldwide. Concentration in both petrochemicals and agrochemicals means that investors can actively engage with a handful of companies to drive forward a systemic transformation in the sector in line with these companies public commitments to sustainability. Investors must engage with established science and the precautionary principle to push for high-level changes in conduct and reporting. A common lobbyist tactic is to drag investors into side issues or the minutiae of individual chemicals, while avoiding the larger issue of systems change and chemical companies’ undermining of public policy and regulation.

Progress towards a more sustainable chemicals sector could start with investors in agrochemical and petrochemical companies ramping up their engagement with the world’s largest chemicals companies by asking these companies to:

- Publicly support cost-effective climate policies in line with the Paris Agreement goals of keeping average global warming to well-below 2°C, with detailed metrics tracking progress, similar to a Transition Pathways Initiative approach. This would require board-level engagement at each company to set targets and integrate them into executive remuneration and long term capital planning decisions.

- Publicly identify technical and financial shortcomings in the agrochemical and petrochemical industry lobbying narrative in support of expanding production of the most harmful chemicals and products. This information is well documented, so investors just have to step up and articulate their position on the need for chemicals companies to operate in a manner that preserves environmental and human health.

- Ensure alignment of public commitments on climate action and biodiversity with the substance of company and industry association engagements with policymakers. Currently lobbying practices show that this is not happening.

- Establish robust governance and reporting procedures on climate risk, biodiversity and environmental protection and associated lobbying by each company and its trade associations, including assignment of board oversight for lobbying alignment. At the largest chemical companies, investors can communicate an expectation that the nomination, remuneration and audit committees play a key role in ensuring that board appointments, pay practices and procedures promote long-term success and climate risk awareness. Climate change, biodiversity preservation and environmental and human health issues related to company product life cycles should have a clear and formal place on the board’s agenda. Investors can then follow-up to make sure company conduct continues to align with public sustainability commitments and that the executive management are seriously assessing these risk areas.

- Assess misalignment between company policies on climate change, biodiversity and human health with their policy engagement record via tools such as those provided by InfluenceMap. Following this assessment, investors should request that management take corrective action to ensure alignment in time for COP26.

- Publicly disclose the company’s position on climate change, biodiversity and environmental protection, and the lobbying of trade associations where it holds membership on these issues. The goal of requesting this disclosure is to enable investors to assess alignment between a company’s public policy statements and their conduct on these issues, including via trade associations.

Join us for the CLAP chemicals sector online investor roundtable on 10 December for a deeper dive into all of these issues.

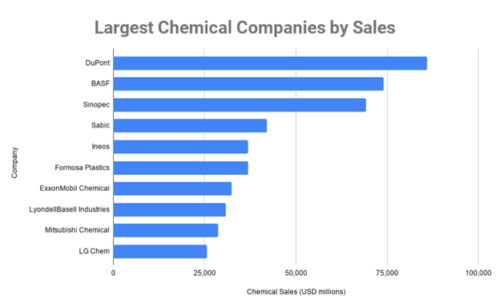

Top 10 global chemicals companies by sales. Investors should engage the largest companies in the sector to push for a system-wide change, including respect for the precautionary principle and more transparent lobbying disclosure across markets. Source: https://blog.bizvibe.com/blog/largest-chemical-companies

Agrochemicals industry seeks to prolong fossil fuel dependence in food production

Pesticides, herbicides, and particularly synthetic fertilisers all play a key role in the fossil fuel-dependent farming systems that have spread rapidly in the past 50 years. The expansion of synthetic chemicals in food production have boosted yields but are also driving climate change, environmental pollution and biodiversity loss.

According to the Center for Responsive Politics, from 1998 to 2020, the agricultural industry spent more on lobbying in the US than the defense industry and engages in many of the influence and lobbying tactics outlined in our earlier sector Discussion Notes. The sector has effective trade associations, with the US-based American Farm Bureau Federation (AFBF) presenting itself as a “unified national voice of agriculture.” While lobbying to block climate action on a number of levels in the United States, the group has also protected the ongoing use of dangerous chemicals by its members. AFBF membership includes the small handful of companies who control the global agrochemicals market: Bayer (acquired Monsanto in 2018), Corteva (formerly Dow and DuPont), Syngenta, BASF and FMC. According to the United Nations Special Rapporteur on the right to food, many of these companies’ pesticides have “catastrophic impacts on the environment, human health, and society as a whole.” Investors have an opportunity to press the global agrochemicals oligopoly to better align their business models with a climate secure future.

“Climate resilient” agriculture from the world’s largest chemicals companies

In response to the climate impacts of chemical heavy agriculture, the agrochemical industry has begun heavy influencing efforts focused on “precision agriculture” and “regenerative agriculture”, using both terms to seek to define a global narrative around “climate smart” and “climate resilient” agriculture that includes growing chemicals use and the adoption of genetically modified seeds. Industry trade associations will not acknowledge the need to phase out meat and dairy as demand for animal feed is driving the hazardous pesticide industry, data reveals. An estimated three quarters of the world’s soya and maize production ends up as animal feed for the meat industry, particularly for chickens and pigs. Industrial agricultural diverts food, water and energy to feed a meat raising industry that is destroying the planet. As mentioned above, pesticides account for around 200,000 acute poisoning deaths each year. So the industry represents short term and long term risks for investors who are committed to climate action and the SDGs. Forceful stewardship and meaningful engagement with the largest companies on their lobbying records should be a priority for investors this year.

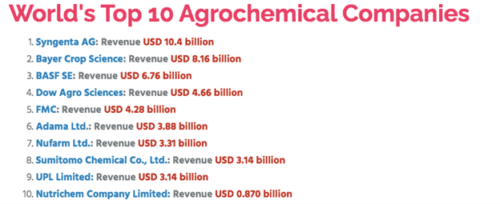

The agrochemicals sector is concentrated creating an opportunity for investors to engage across the sector with shareholder resolutions on a Paris-aligned business transition plan. Source: Market Research Reports.

The agrochemicals sector is concentrated creating an opportunity for investors to engage across the sector with shareholder resolutions on a Paris-aligned business transition plan. Source: Market Research Reports.

Beyond agrochemicals: the global plastics & petrochemical industry

Plastic pollution has increased tenfold since 1980, 300-400 million tons of heavy metals, solvents, toxic sludge and other wastes from industrial facilities are dumped annually into the world’s waters, and fertilizers entering coastal ecosystems have produced more than 400 ocean ‘dead zones’, totalling more than 245,000 km2, an area larger than that of the United Kingdom landmass. This fountain of plastic is fueled by a small group of players in the upstream oil and petrochemical industries who are betting their future growth prospects on demand for plastics. But if Paris Agreement climate targets are any guide, and the push to a circular system, or at least higher rates of recycling are effective, there is significant potential for stranded petrochemical capital expenditure. The IEA and a number of oil and gas companies see petrochemicals as a large driver of expected oil demand, in spite of plastic’s climate impacts, health costs, waste management and disposal, and ocean pollution. The industry has been aware of all these risks for some time, particularly ocean contamination by plastic and has yet to be held to account by investors.

ExxonMobil, BASF, Eni, INEOS, and Dow are the biggest plastic producers worldwide, and should be engaged using all of the forceful stewardship tools available to investors. As the world prepares for COP26, investors must engage in the systemic transformation of the chemicals sector in line with their public commitments. Starting with sector wide business transition shareholder resolutions at the 10 largest chemicals companies in 2021 would be a good way to start.

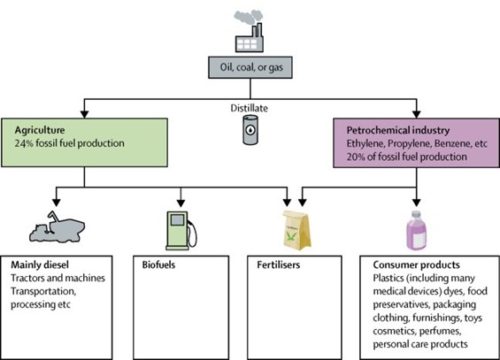

The upstream fossil fuel sector feeds global agrochemical and petrochemical industries. Targeted investor engagement in the upstream fossil fuel sector and with the 10 largest chemical companies could begin to bring about the necessary transformation in line with Paris Agreement targets. Source: Demeneix, B. (2020): ‘How fossil fuel-derived pesticides and plastics harm health, biodiversity, and the climate’ https://www.thelancet.com/journals/landia/article/PIIS2213-8587(20)30116-9/fulltext