Align and Conquer: two things to do right away – from the Corporate Lobbying Alignment Project

Some of the world’s largest asset managers are beginning to address corporate policy capture risk, but it’s too slow. This blog post shares a selection of key lessons from the Corporate Lobbying Alignment Project (CLAP) report card for asset managers and other stakeholders in the institutional investment system who want to better address lobbying risk. The report is available here.

12 steps for the world’s largest asset managers to tackle policy capture risk

The CLAP, our year long research project on investors and corporate policy capture, showed a lack of established (best) practice on corporate policy capture in the finance sector. In response, we proposes 12 steps for asset managers and asset owners to more consistently curtail negative lobbying practices, across three areas for intervention:

(a) better data & disclosure on all forms of lobbying and influence spending, including political finance;

(b) changing behaviours – both internally with a consistent policy on lobbying and trade association alignment, and externally via stewardship with investee companies; and

(c) making stronger arguments to regulators, public policymakers, and investor peers on the need to address systemic risks, and policy capture risk.

The 12 action points are intended to engage a public debate and inform structured internal action plans by investors and their networks to create a consistent approach to lobbying. They make clear what needs to be done. Yet our report card shows investors have yet to take corporate policy capture seriously: 78% of the world’s top 50 asset managers by AUM received a D or E. This includes household names such as Amundi, Blackrock, Nuveen or Royal Bank of Canada. For those who claim to be serious about addressing systemic risks to financial stability, now is the time to start addressing systemic risks linked to negative lobbying.

The good news is that asset managers understand systemic risks. They have the stewardship tools required to address policy capture and coordinated corporate lobbying and they themselves are skilled at engaging with regulators. And this is a good place to start. Here are two important steps.

Step 1: building coherent internal policy on lobbying & influence

Research and interviews with asset managers revealed the importance of creating a coherent internal policy to define a process for sharing information on lobbying conduct and trade association membership across the organisation. It becomes a building block to an effective and consistent external engagement strategy on lobbying alignment with portfolio companies and regulators. Our analysis shows that less than a third of the world’s 50 largest asset managers publicly disclose their own trade association memberships, leaving significant room for improvement in organising and sharing this information.

For those managers who already have an internal policy on lobbying conduct, our report card supports leaders in pursuing these important discussions internally. They know that investors who have committed to support action on climate change for example, or who have spoken out on risks to democracy in the US need much better alignment between these commitments and their own lobbying conduct.

ESG leaders in asset management should engage their in-house counsel and public affairs teams and work together to create a coherent policy on lobbying alignment. At present, information on asset manager trade association membership and lobbying conduct, including spending on political finance and informal influence channels, is spread across the organisation. ESG and stewardship teams rarely have immediate access to this information and cannot readily confirm that a fund manager’s trade association membership and activity aligns with their stated ESG objectives.

Step 2: concentration of lobbying spending in key sectors can help to focus engagement

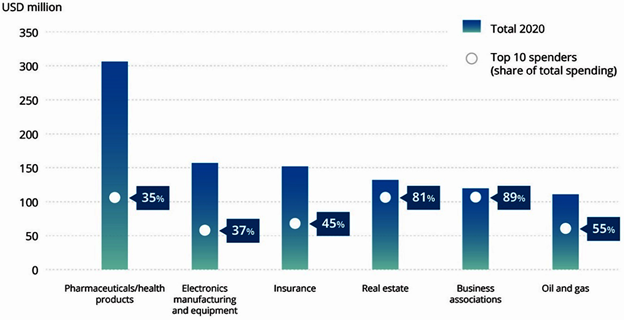

Beyond internal alignment, asset managers can communicate expectations on the need for lobbying alignment more clearly with investee companies (especially but not exclusively during the proxy season. This need not be onerous: he concentration of lobbying spending is significant, meaning that engagement with a small handful of large companies across key sectors could have a significant positive impact: Our research showed that concentration of market and lobbying power in the top 5 listed companies is significant for a range of sectors with systemic ESG impact. This means that investors can focus their engagements on a small number of companies to have a global impact. In addition, the OECD’s recent analysis on lobbying in the United States highlights that registered lobbying spending is also concentrated, with the top ten company and trade association spenders accounting for up to 90% of the total expenditure on lobbying in their respective industries.

Image via OECD: https://www.oecd.org/governance/ethics/lobbying-21-century.htm