The US AGMs: which investors matter the most?

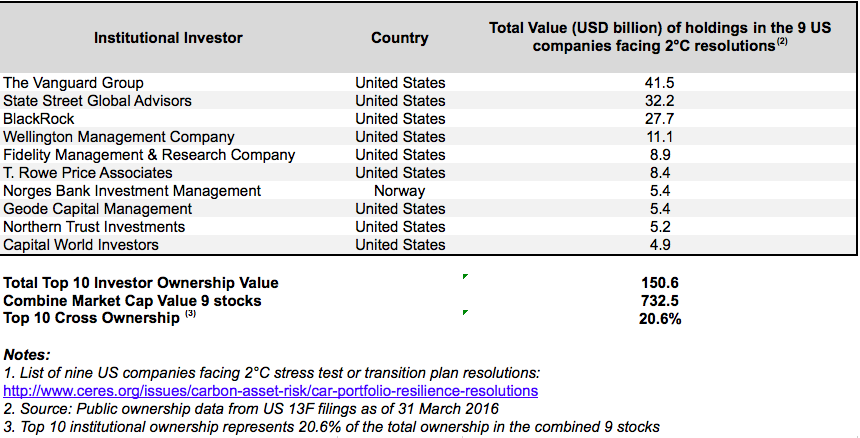

Preventable Surprises has undertaken an analysis of who owns the nine companies in the USA that are facing 2°C stress test / transition plan resolutions.

One highlight of this analysis is that the 6 largest investors on the list – the Vanguard Group, State Street Global Advisers, BlackRock Institutional Trust Company, Franklin Advisers, Fidelity Management & Research Company, and T Rowe Price – together represent more than 50% of the combined ownership of the top 50 investors in these companies.

In dollars, the top 6 investors have a $130bn stake in these 9 companies of the total $248bn owned by the all the top 50 investors put together.

In overall relative terms, the top 6 (and the top 50) institutional investors represent 18% (and 34%) respectively of the combined market cap ($732.5bn) of the nine companies.

Ceres and Funds Vote have created a league table of investors based on their voting records on climate resolutions. Several of these top 10 investors – including Blackrock, Fidelity, State Street and Vanguard – are in the lower half.

In contrast, Norges Bank Investment Management, has actually pre-declared that it will vote for the 2°C resolutions at Chevron and Exxon. The declaration on the Southern 2°C resolution is awaited.

Our conclusion? The support of investors in this top 10 list will be decisive.

If they do what large US mutual funds tend to do – which is to reflexively vote with management on climate issues (i.e. AGAINST), or even if they ABSTAIN – it will be very difficult for “climate aware” investors to ensure the resolution passes and that the companies manage climate-related risks well.

We believe investment managers have a fiduciary obligation to vote proxies in a manner consistent with informed management of long-term economic risks to which the fund is exposed from stranded assets and related market changes resulting from recent developments. Moreover, we see little justification for voting inconsistently on the effectively the same resolution in different markets, especially if this is simply to “support management”. The argument that voting is not needed because of influence that can be exerted “behind closed doors” is unverifiable and in this post COP21 context, unconvincing. Private engagement is definitely needed – not least to align executive pay with a 2C transition plan – but this does not remove the need to vote for these 2°C stress test / transition plan resolutions.